Real Estate Bubble Index

Key Takeaways

- The Swiss investment bank UBS published its annual global real estate bubble index report in October 2022

- UBS evaluates the risk for a real estate bubble higher than ever before because of the high price-to-rent ratio

- Higher mortgage rates bring down profitability for real estate investors leading them to sell properties, UBS argues

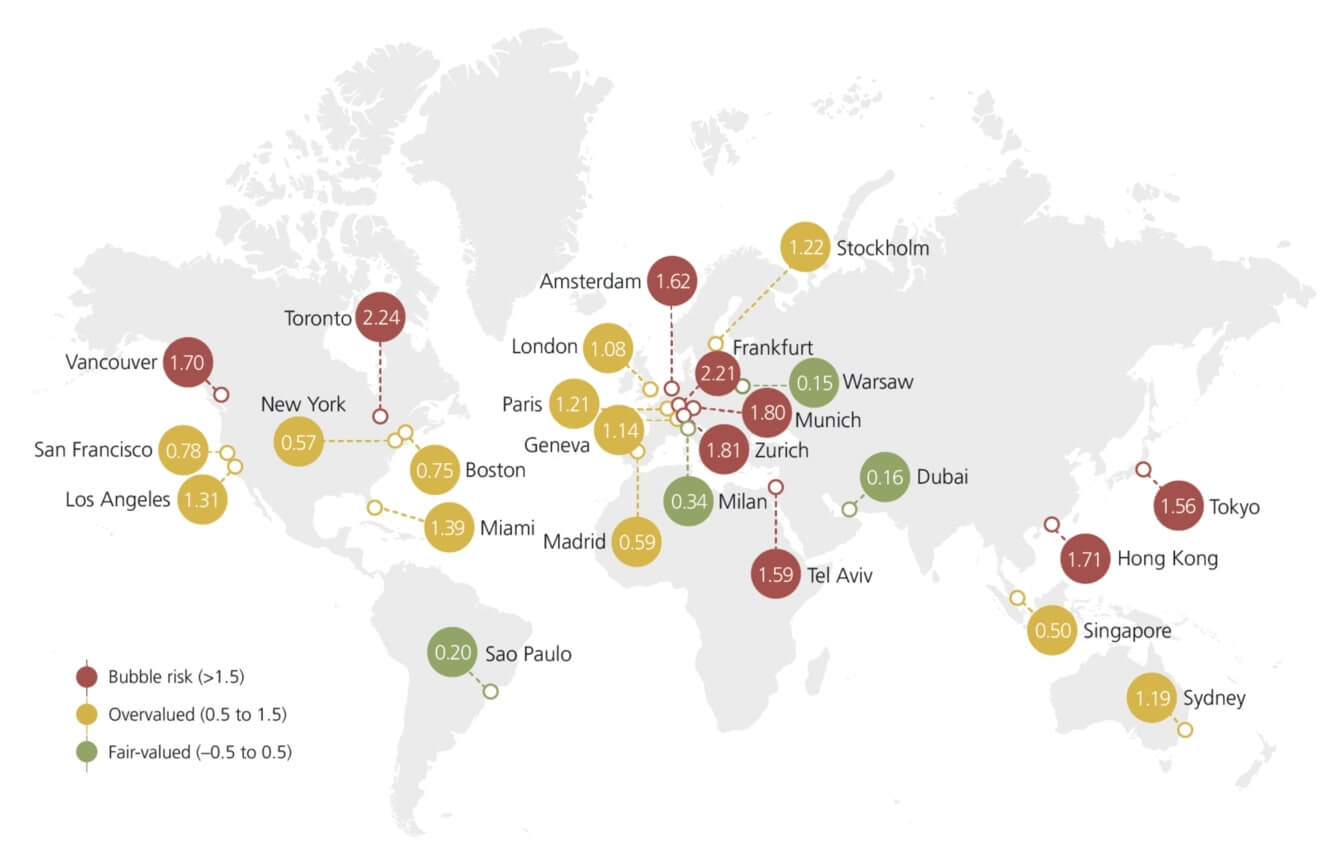

- 2 out of the top 4 cities with the highest real estate bubble risk worldwide are Frankfurt and Munich

UBS Global Real Estate Bubble Index Explained

In October 2022, the Swiss investment bank UBS published their yearly Global Real Estate Bubble Index again, comparing property prices all over the world to show the cities with the highest bubble risk.

2 out of the top 4 cities with the highest real estate bubble risk worldwide are German cities: The A-locations Frankfurt and Munich (as seen in the graph on the right).

This post of the GermanReal.Estate blog will examine in detail why UBS ranks the 2 German cities Frankfurt and Munich so high on their global real estate bubble risk list.

Because if you live in Frankfurt or in Munich and experience rent prices and property purchase prices firsthand, you might have a different than UBS (our business is in Munich too).

UBS opens its global real estate bubble index with the very important sentence “In many cities, there is not enough housing supply” which is especially true for many cities in Germany.

This is also one major argument against the real estate bubble. In order to have any bubble, you would need a supply that is far above the demand so prices fall.

UBS acknowledges there that is no excess supply in many cities around the world. They build their real estate bubble on two arguments: Development of rents & mortgage interest rates.

Real Estate Bubble Reason 1: Price-To-Rent Ratio

The first argument for UBS supporting the rising real estate bubble risk is the development of rent prices compared to the development of property prices. In all major cities around the world, property prices went up and up over the last years or decades, in some cities even by double-digit growth rates (+10% per year).

While property prices increased a lot all over the world, rents increased as well but only with local salaries. Resulting in property prices that have outgrown rent prices.

The real estate bubble argument is, that the higher the difference between property prices vs. rent prices, the lower the profitability for real estate investors. And the lower the profitability for real estate investors, the harder it is to justify high property prices.

The prominent “price-to-rent ratio” calculates the discrepancy between property prices vs. rent prices. The graph on the right shows how many years a property needs to be rented out in order to pay for itself.

The no. 1 cities with the highest price-to-rent ratio are the cities with the lowest profitable real estate: Munich, Hong Kong, and Tel Aviv. In all these 3 cities, investment properties must be rented out for 44 years until they have paid for themselves. Frankfurt is #4 on the price-to-rent ratio list with 42 years until your property would have paid for itself with passive income from renting it out.

All price-to-rent ratios from the current global real estate bubble index 2022 are vastly higher than those from 2012 (except Singapore, Madrid, and Dubai) giving an argument supporting a higher real estate bubble risk than 10 years ago. What are high price-to-rent ratios telling us? That investors are willing to sacrifice passive rental income in the hopes of further increasing property prices (driven by historically low mortgage rates).

Cities With The Highest Real Estate Bubble Risk Worldwide

Real Estate Bubble Reason 2: Mortgage Interest Rates

Continuously increasing price-to-rent ratios can only be justified by historically low mortgage interest rates (according to UBS). Over the last +10 years, central banks around the world have been lowering interest rates to 0% in order to boost the economy.

During the time of 0% interest, investors were looking for profitable investments as savings accounts and fixed-term savings accounts returned almost no profit. Therefore driving up prices of stocks (e.g. REITs), ETFs, and real estate (crowdfunding).

In early 2022, central banks started to raise their interest rates again (and mortgage rates with it). The current realistic mortgage rate in Germany can be seen in the table below:

Rising interest rates are not beneficial for real estate investors, UBS is certainly right here. But mortgage rates are no isolated factor that is detached from other factors that influence real estate prices:

- What are alternative investments?

- How are (real) incomes developing?

- How high is the inflation rate?

When adjusting for inflation, property prices developed as seen in the chart on the right. Even though real estate valuations increased in Frankfurt and Munich on a nominal basis, real property prices fell in both cities when adjusted for inflation.

Real estate prices have become increasingly unaffordable but you would like to benefit from higher interest rates? Check out our real estate security tokens that our investors can trade on the blockchain.

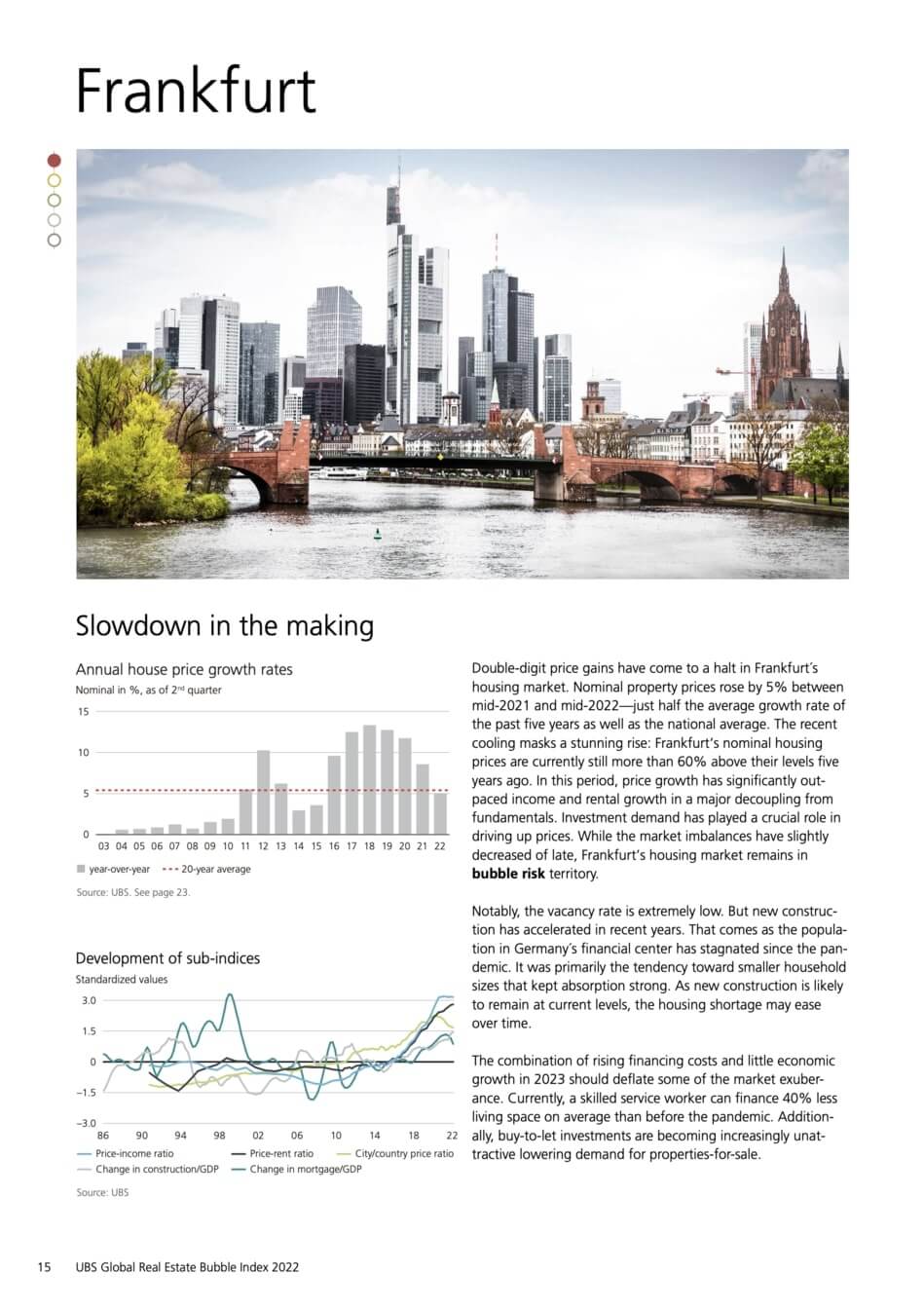

Frankfurt Real Estate Bubble Index

One of the 7 A-class cities in Germany even got its own page in the UBS global real estate bubble risk index: Frankfurt. UBS is seeing a high risk of a bursting bubble here and titles the page “Slowdown in the making.”

The annual growth chart of property prices in the middle of the page shows clearly that Frankfurt was the big winner of Brexit, as a lot of high-paying jobs in the finance sector moved from London to Frankfurt.

The growth chart that showed an almost 15% increase in property valuations in 2017, 2018, and 2019 slowed down significantly and is expected to be below the 20-year average growth rate of +5% in 2022.

UBS argues that the increase in property prices has to slow down at some point as rents did not keep up with property prices (as seen in the price-to-rent ratio above).

You can download the full global real estate bubble index report of 2022 on the website of UBS here in case you would like to dig deeper into the real estate bubble discussion yourself.

At the same time, UBS argues that property prices could rise even higher as vacancies are at an extremely low level in Frankfurt. The Swiss investment bank expects the housing shortage will resolve itself in the next years, which we are highly doubting given the low amount of living space Germany is actually creating (and has been creating over the last years).

That is why we are still confident that real estate will continue to be an exciting and profitable investment over the long term. If you share our opinion and want to invest in German real estate in the easiest way possible, then see what kind of real estate security tokens are currently available on our marketplace.

Pingback: Immobilienblasen Index - GermanReal.Estate

Pingback: REITs In Germany | GermanReal.Estate

Pingback: How Inflation Impacts Real Estate Investors | GermanReal.Estate

Pingback: Passive Income & Real Estate: Is That Possible? | GermanReal.Estate

Pingback: Location Ranking (A, B, C & D) | GermanReal.Estate

Pingback: Global Real Estate Crash In 2023? | GermanReal.Estate

Pingback: 2 Reasons For Rising German Property Prices | GermanReal.Estate

Pingback: Will The German Housing Market Crash? | GermanReal.Estate

Pingback: Rising Real Estate Prices - Here Are the Best Tips! | GermanReal.Estate

Pingback: Invest Money in Securities - We Can Help You! | GermanReal.Estate

Pingback: Real Estate Crowdfunding | GermanReal.Estate

Pingback: German Real Estate Market Explained By A Real Estate Developer

Pingback: German Real Estate In 2023 | GermanReal.Estate

Pingback: Real Return of the German Real Estate Market | GermanReal.Estate

Pingback: The Truth About the German Real Estate Boom: Supply, Demand, and Growth

Pingback: Is Germany in a Real Estate Bubble? | GermanReal.Estate