How Inflation Impacts Real Estate Investors

Key Takeaways

- Inflation in the Euro area is at an all-time high. Investing in real estate might be the perfect solution to fight inflation.

- When saving UP (with e.g. ETFs), you are slowly growing your investments and inflation is working against you.

- When saving DOWN (with real estate), you take a mortgage from a bank so inflation works in your favor.

- Everyone with debt is profiting from high inflationary times while everyone with assets is losing money.

Inflation In The Euro Area

Our European Central Bank is targeting an inflation rate of 2% in the Euro area. We started 2022 with a 5% inflation and climbed to more than 10% inflation in October and November of 2022 (see graph below). All while interest rates from banks are still near 0% (for savings accounts, not for mortgages). If your money loses basically 10% in value year over year, what can you do in order to fight inflation? 🤔

Before we come to possible solutions, it is important to understand that there is absolutely nothing anyone can do against inflation itself. The inflation rate in the Euro area will rise or fall without any single person having a significant influence on that. The only thing you can do to fight inflation is to protect your hard-earned money by investing it in real assets:

- Equities like stocks or ETFs

- Commodities like Gold or Silver

- Blockchain-based investments like cryptocurrencies or security tokens

- Real estate (investment properties or homes for self-use, not REITs)

All possible investments above work the same way with the exception of real estate. Real estate is the only investment that allows you to take a loan from a bank. Good luck trying to convince a (German) bank to give you a loan in order to invest that money into cryptocurrencies or stocks. And this difference makes real estate such a perfect hedge against inflation because it allows you to save DOWN instead of saving UP.

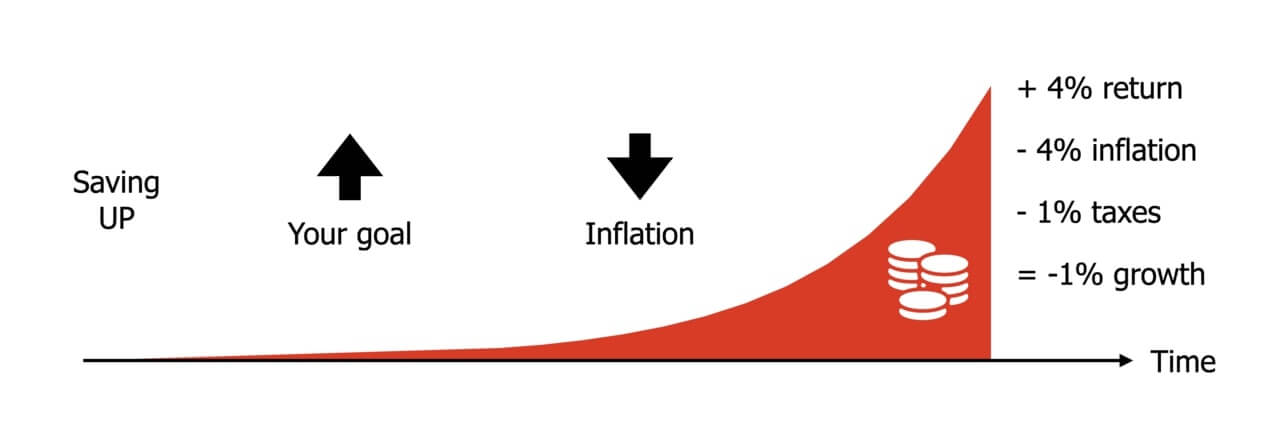

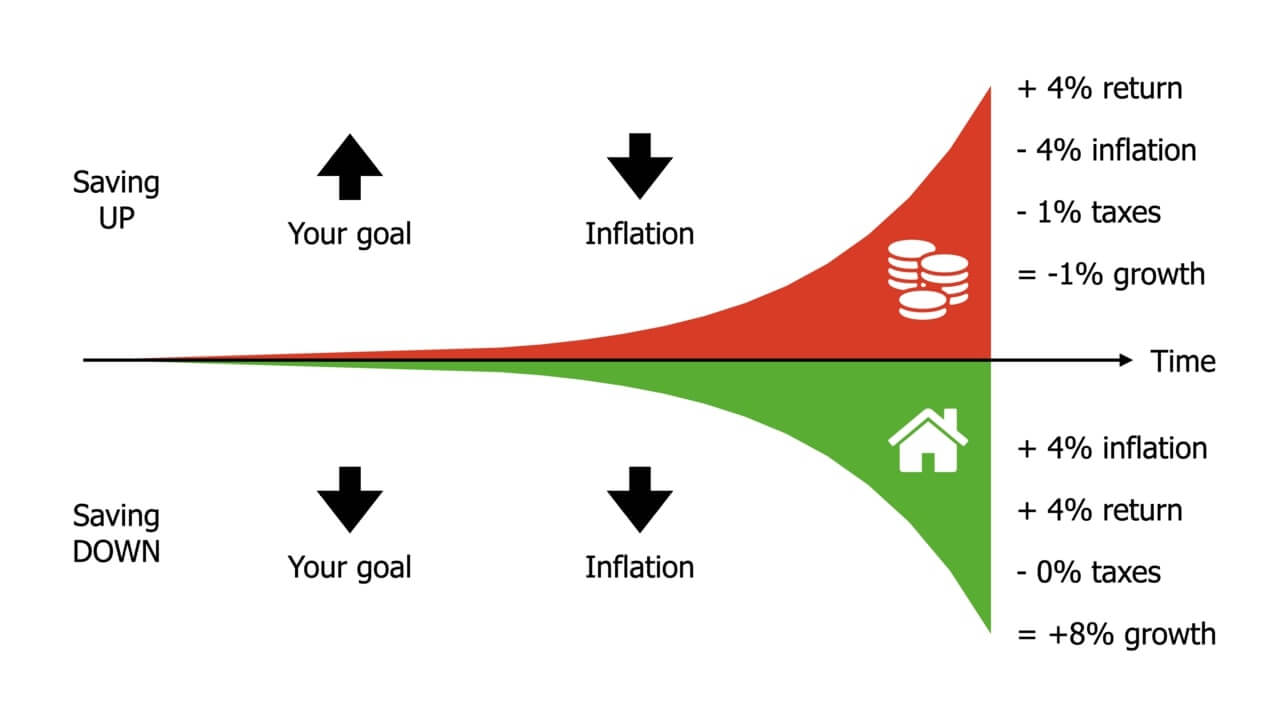

Saving Up: Inflation Is Your Enemy

When investing in any type of savings plan (e.g. stocks, ETFs, cryptocurrency, real estate crowdfunding, etc) you are starting from 0€ and invest gradually more money over time. When you invest 100€/month, you have 1.200€ in your account after 1 year or 12.000€ after 10 years. If you don’t let your money sleep in a bank account but invest it with a meaningful return, you will profit from exponential growth (“compounding interest“) as seen in the graph below.

While there is generally speaking nothing wrong with saving UP, we have to understand that inflation is fighting against us here. While your goal is to save more and more, inflation is bringing the value of your money down (currently by ±10%/year). The example below shows that you need a rate of return far above the inflation rate in order to have a real positive investment return.

Example of saving UP:

- You are investing money (saving up) with a 4% rate of return (from portfolio growth or passive income from rents)

- The inflation rate is at the same time at 4%, leaving you with a 0% realistic rate of return

- Your 4% rate of return is taxed with at least 25% capital gains tax, leaving you with a -1% investment return

Saving up and investing your money is far better than leaving all your money in a bank account with 0% interest, but the example above shows that you are just fighting windmills when saving up. If your (net!) investment return is smaller than the inflation rate, you are actually losing money while you think that you are getting richer. If saving UP is not the solution, maybe saving DOWN with real estate might be better.

Saving Down: Inflation Is Your Friend

How about instead of fighting inflation by saving UP (which you cannot win anyway), you make inflation your friend by saving DOWN? All you need to do is to work in the same direction as inflation, trying to devalue your money as fast as possible. And how do you do that? By taking a mortgage from a bank and getting into debt to buy a German property.

With a mortgage, you don’t start saving at 0€ as you do with a savings plan that is saving up, you start at 100.000€, 200.000€, or whatever your property value is. While you get a tiny profit with a savings plan that returns 4% in the first year, you get an enormous profit by investing in a property that returns 4% in the first year (4.000€ for every 100.000€ in property value). And you are not even taxed on your profit with real estate if you are holding your property for +10 years (tax-free speculation period in Germany).

Real estate investors are not just profiting from rising property prices, they are also earning more money the higher the inflation rate is (even if the real estate “bubble” is bursting). The nominal value of your mortgage will stay the same (100.000€ mortgage will stay 100.000€ mortgage), but the more you fast forward in time the more you will pay off your mortgage with devalued Euros (adjusted by inflation). In times of 10% inflation, your mortgage is basically getting 10% “cheaper.”

Is Real Estate The Perfect Solution Against Inflation?

If you want to profit from inflation while everyone else is losing, you can do it! You just have to go into debt, it’s “just” that easy. 🫠

Jokes aside. In order to profit from inflation, you need to get out of cash that is losing value fast and start investing in real assets like stocks, ETFs, or real estate. The major advantage of real estate is that you can go into debt when making that investment which will boost your return even further the higher the inflation rate is. But please don’t go into bad debt (e.g. consumer loan), only go into good debt (e.g. mortgage).

We realize it is not so easy to just go out and find a good investment property and that is why we created GermanReal.Estate to make your real estate investor life as easy as possible. With our real estate security tokens you don’t need to find the right property in the right location for the right price. You can just register as an investor and see what investments are currently available on our marketplace.

Pingback: Wie die Inflation sich auf Immobilieninvestoren auswirkt - GermanReal.Estate

Pingback: 2 Reasons For Rising German Property Prices - GermanReal.Estate

Pingback: Global Real Estate Crash In 2023? - GermanReal.Estate

Pingback: Passive Income & Real Estate: Is That Possible? - GermanReal.Estate

Pingback: Where Are Properties In Germany Still Affordable? - GermanReal.Estate

Pingback: Mönchengladbach: Welcome Home Security Token - GermanReal.Estate

Pingback: REITs In Germany - GermanReal.Estate

Pingback: Why Are We Using The Blockchain Technology? - GermanReal.Estate

Pingback: Special Purpose Vehicle (SPV) - GermanReal.Estate

Pingback: Real Estate Bubble Index - GermanReal.Estate

Pingback: Will The German Housing Market Crash? | GermanReal.Estate

Pingback: Rents In Germany | GermanReal.Estate

Pingback: How Can I Earn Money On GermanReal.Estate? | GermanReal.Estate

Pingback: Security Token | GermanReal.Estate

Pingback: Real Estate With No Money | GermanReal.Estate

Pingback: German Real Estate Market Explained By A Real Estate Developer

Pingback: Best Real Estate Locations In Germany Until 2030 | GermanReal.Estate

Pingback: German Real Estate In 2023 | GermanReal.Estate

Pingback: Real Return of the German Real Estate Market | GermanReal.Estate

Pingback: Top 10 Most Expensive German Cities For Real Estate Investments

Pingback: How Real Estate Can Make You Rich - Exploring Investments

Pingback: Surprising: Rents In Germany Are Getting "Cheaper" | GermanReal.Estate

Pingback: The German Real Estate Market: Is a Crash Happening Now? | GermanReal.Estate

Pingback: The Rise and Fall of Vonovia - Europe’s Top Real Estate Company | GermanReal.Estate